The Weekly Random Walk – July 17, 2023 From Stephen Colavito

An Aggregation of Various Economic, Market Research, and Data

The Boomerang

As kids, some of us were allowed to make bike ramps and given boomerangs to throw in the front yard (back in the days when kids were encouraged to do stupid stuff, so we learned). Throwing a boomerang either meant you hit another kid, broke a neighbor’s window, or got a concussion trying to catch it as it came back around and hit you in the head.

Parents were assured by their children that they knew what they were doing, but inevitably after a visit to the emergency room, it was taken away.

This week, we reflect on boomerangs thrown by the Fed and ourselves, which have come back to thump us in the head.

That’s Got To Hurt

As the market continues to rally, those on the short side of the market are getting smacked in the head. As those shorts have had to cover, the short squeeze in the equity market may be getting close to being done. Over the last month or so, according to CFTC data, spec short positions in the S&P futures have been cut at the fast pace in three years. In addition, data from Morgan Stanley suggest a similar dynamic has taken place in the ETF market, where shorts as a percent of market cap have dropped to the bottom end of the three-year range. Single-named shorts (in individual positions) are still somewhat high.

I had discussions with PMs at several hedge funds this week, and the ones we talked to are lagging in performance because they have been net neutral on the market this year (long/short pairing). It has always made us nervous when markets are not balanced (net longs against net shorts). Currently, the market is skewed to the net long side of the market.

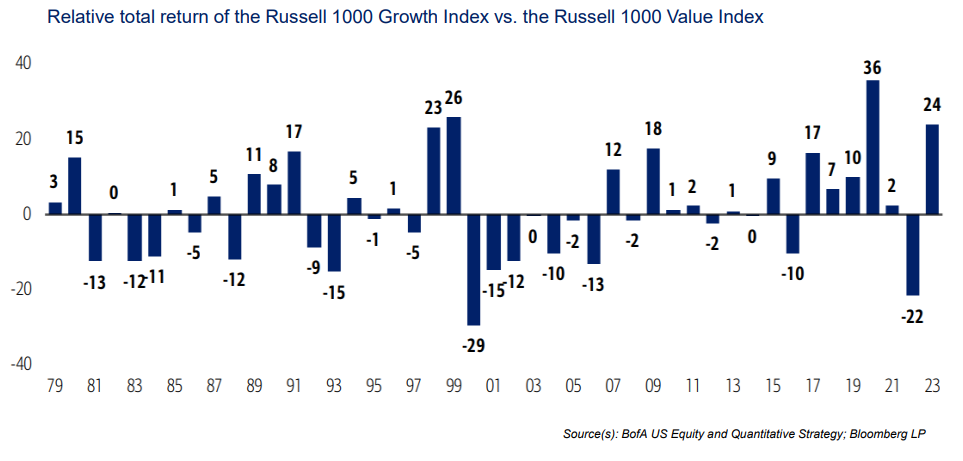

That Came Back Quickly (Puns aplenty)

The Russell 1000 Growth Index is 24% ahead of the Value Index through June 30th (29% vs. 5%), more than reversing its 22% underperformance last year (-29% vs. -8%). This is again driven by the big seven stocks, which (surprise) also make up a disproportionate amount of the Russell 1000. This boomerang in performance and the market’s tone change continues as investors think growth will drive the economy over the next 6 – 12 months.

Wide Side

Over the last year, a steady negative correlation has been between tech performance and real rates (rates less inflation). However, this has reversed over the last few months, as 10-year real rates hit highs of 1.76% while nonprofitable tech has rallied. Real rates have declined this week with the bond rally, but tech continues to rally and create a wider spread between the two. A spread this wide is abnormal and wider than historical norms.

That’s Got Some Shape

As we have discussed before, since the 1960s, the US yield-curve inversions have predicted all eight US recessions, which begin roughly one year in advance. The yield curve’s forecasting record (unlike economists) since 1968 has been perfect. Not only has each inversion been followed by a recession, but no recession has occurred without a yield curve inversion. So, it’s a little confusing to us how so many on Wall Street are now calling for a soft landing.

The yield curve’s predictive prowess is chronically misunderstood and misapplied, even by forecasting pros and the supposedly sophisticated financial media that cover them, as illustrated in two recent essays by James Mackintosh in the WSJ who (like many journalists in the MSM), always have opinions but seldom uses facts.

Since the probability has been 100% since the early 1960s, we are sticking with our call of recession in late 2023 or early 2024 based on the inverted yield curve. Maybe “this time is different, but we don’t think so.

Walk About

Recency bias likely means most investors are working off the recession playbooks of the near past. That means stocks would sell off at the beginning of signs of recession before the Federal Reserve returns and throws a life preserver back to the market (via lower rates). This year, the rise in P/E multiples has driven the market higher (led by AI-type stocks).

Recession(s) generally adversely affects profit margins and revenues for most consumer-facing companies (consider the recent headlines with Disney having fewer people go to their theme parks). A decline in revenue means a decrease in P/E (earnings).

We have been wrong in our call for a pull-back in the indexes. There is still over 1 trillion dollars in cash, and some of that money continues to come into risk assets. Our thesis was that the market would get “ahead” of higher yields, a slower economy, and valuations would reset (before the recession). But with M2 still accommodative, that call has boomeranged on us and smacked us in the head (and wallet).

We realize our advice has given up some performance for those who trade. For those who invest, you’re still in the markets and have seen growth. But despite being wrong on timing, we think the upside of equities is limited as P/Es continue to climb. We still believe traders will have a chance to make money in 2023.

“Do the Harry”

For those of you who have never heard the saying, Google it, but the US government is “Doing the Harry” right now regarding debt. As seen by the St. Louis Fed, the US Government is on track to pay more than one trillion dollars (with a T) annually in debt interest by the end of 2023. This continues to erode discretionary spending by Washington but, more importantly, will lead to 1) higher taxes (less consumer spending) and 2) benefits being taken away from taxpayers.

Just look at France and all the riots in that country to see what life will be like in the US if both parties don’t wake up on Capitol Hill.

Before we even finished that last point, news hit that the Biden administration now forgives 39 billion dollars in student debt for over 800,000 borrowers. After the Supreme Court struck down Biden’s first attempt at forgiving student debt, the administration has figured out a reach around, sorry, work around via the Department of Education.

The tweaks that created the loophole include counting payments for borrowers who had paused their payments in various deferments and forbearances and those who made partial or late payments.

We wonder how all those taxpayers who never had the chance to go to college think about paying for someone who did. It is another way for lawmakers to add to a growing debt that will eventually suffocate the economy, the government budget, and the king dollar.

“Onya bike. Tell your story, walkin’.”

With all the spending on nonsense like Ukraine, student loans, pork, etc., it seems as if those who don’t have homes in the US have been left behind. New data from Bloomberg shows that the number of families experiencing homelessness skyrocketed this year across 20 major cities.

The nationwide family homelessness contradicts the administration’s claim that “Bidenomics” has unleashed a new era of prosperity. The study found that a shocking 72,700 people in families with children were homeless in 20 cities across the US (as of January), a massive 36.6% jump from a year before.

This problem doesn’t fall just on the shoulders of Democrats; both parties have overlooked those in need in the US. In fact, in a recent interview, when pressed about the economy being degraded, higher suicide rates, public disorder, and crime exponentially increasing, former Vice President Mike Pence’s response was, “That’s not my concern.”

We realize that was out of context, but we also realize there is truth to that statement from many in DC.

When It Boomerangs, Things Break (Bullet Points)

As we forecasted several months back, the so-called BRICS countries and their currency trading system made another step forward in grabbing share away from the US-backed SWIFT system. They announced they are planning on introducing a new trading currency that will be backed by gold. More details are expected next month at the BRICS summit in South Africa, but the continued acquisition of gold bullion by these member nations makes more sense after the announcement.

This system continues to make inroads in building a platform that will challenge the SWIFT and Petrodollar system. Despite jawboning by the Treasury, they are not concerned about the positioning of this new platform; several insiders (off the record) have shared views that are not in line with the narrative coming from the department. Dethroning the dollar will take years, but one has to wonder when the government will change its position on the competition.

With the cooler-than-expected CPI print, the equity market is moving higher on momentum. The market’s strength has caught us by surprise based on fundamentals. But having been in this game for 30 years, we know that fundamentals don’t always work. Sometimes its liquidity and momentum lead markets forward.

There is nothing seems to be getting in the way of the market potentially moving from the 4505 level (today) to 4650. We are in “nose-bleed” territory regarding valuations, but it seems as if the market isn’t going to take the Fed or its determination to stamp out inflation seriously. With that being said, we believe the catalysts to a market “correcting” to opportunistic levels are going to come when earnings “correct” with a slowing (recession) economy. That may come at the end of the third quarter or possibly early into 2024, depending on the continued strength of the US consumer.

For what it’s worth, we are not alone in our forecast. In discussions with PMs at some substantial hedge funds, their performance is flat YTD as they sit in a “neutral” position waiting for fundamentals to boomerang back to them.

Only time will tell. In the meantime, be nimble in your trading.

No update next week. There will be a “Week In Review.”

Stephen Colavito

Chief Investment Officer

San Blas Securities

stephen.colavito@sanblas-advisory.com

General Disclosures

This research is for San Blas Clients only. The opinions represented in this research are that of the CIO, not advisors or officers of San Blas Securities. This research is based on current public information that we consider reliable, but we need to represent it as accurate and complete, and it should not be relied on as such. The information, opinions, estimates, and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate. Some research can and will be published irregularly as appropriate in the analyst’s judgment.

This research is not an offer to sell or solicitation of an offer to buy a security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or consider our clients' particular investment objectives, financial situations, or needs (individual or corporate). Clients should consider whether any advice or guidance in this research suits their specific circumstances and, if appropriate, seek professional advice, including tax advice. Past performance is not a guide for future performance, future returns are not guaranteed, and a loss of original capital may occur. More information on San Blas Securities is available at www.sanblassecurities.com.