The Weekly Random Walk – December 20, 2023 From Stephen Colavito

An Aggregation of Various Economic, Market Research, and Data

Santa Claus & 2024

We started writing this last week, but because data was changing rapidly, we paused and decided to post our update mid-week. This is the last update for the year, and we will resume in 2024!

This week’s theme is a look at current data (which has been Santa Claus for equities) and our outlook for 2024. Granted, it’s a bit of a mash-up, but we think it will give you our thesis for positioning and expectations.

You Better Be Good For Goodness Sake

Equity markets have been increasing since November, and financial conditions are helping. According to the Bloomberg US Financial Conditions Index, US financial conditions have been the most accommodating since the Fed started hiking rates last year. The Federal Reserve knows conditions have improved, possibly delaying rate cuts beyond current market expectations.

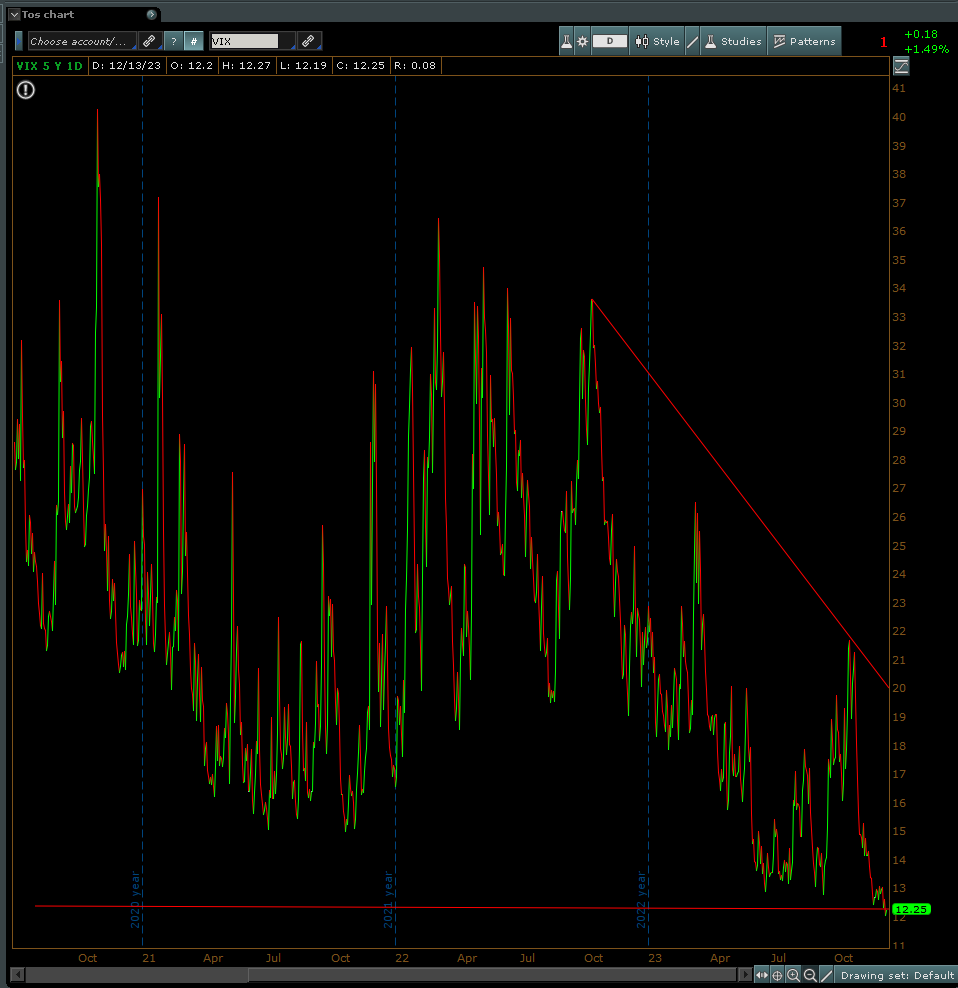

The volatility index (VIX) has dropped like a stone since September. The VIX, or “fear gauge,” has plunged to a four-year low and is a sign of confidence (over) in equity markets. The VIX has tumbled 28% this quarter, a sign of a “Goldilocks” forecast for the economy and markets.

Three Wise Men

We don’t know about frankincense and myrrh, but we know Central Banks bought over one thousand tons of gold in 2023. This would be the second year with over one thousand tons purchased, with 2022 being the first.

Currently, central banks hold just 20% of their reserve in gold. Historically, central banks have about 40% of their reserves in gold (on average). But that figure is low with money printing by global central banks over the last several years.

China is the largest buyer of gold, followed by India, Russia, and Turkey. There is nothing to make us think this is going to slow in 2024. We still like this gift from the wise men.

Santa (aka Chairman Powell) Is Handing Out Gifts For Christmas

Global monetary policy has shifted from tightening to easing within the last few weeks. Chairman Powell pulled a “Powell Pivot 2.0” with his dovish comments after last week's FOMC meeting. Bank of America has followed this shift, and developed and emerging markets are forecasted to have lower rates in 2024. The Federal Reserve is expected to cut rates by 1.50% (150 bps), and their pivot is attributable to a decline in inflation across the globe rather than a rapid deterioration in the economic outlook.

Naughty List

Despite the monetary gifts being handed out, there is more than meets the eye (and the Fed knows this). Based on various data points, the consumer is struggling, and those with credit available are leveraging themselves even more.

If President Clinton is right, “It’s the economy stupid,” it may explain why the current administration sees falling polling numbers despite the Press Secretary saying, “It’s the best economy in ten years.”

These two data points continue to worry us. 1) Credit card defaults are still rising faster than at the peak of the financial crisis. This is happening at a time when credit card debt has just hit new highs (and is setting the stage for economic shock). This is highlighted in the first chart below. 2) Housing defaults are now at the highest levels in a decade. We have been told that housing prices are holding up despite higher rates. Although banks are less leveraged than in 2007-2009, multifamily is the bedrock of housing, which is not a good sign. See the second chart below (Game of Trades sources both).

Foreign Grinch(s)

October saw the second biggest month of foreign selling of both equities and US Treasuries. The selling of Treasuries by Sovereign Entities continues as the US Debt now tops 34 trillion dollars. As the debt continues to rise and China continues to move forward with BRICS and alternative currencies for trade, private buyers are going to have to pick up the slack, otherwise, over time, we could see pressure to rates despite the Fed lowering Fed Funds.

Happy New Year

Despite the recent pivot, the path to a soft economic landing the market wishes for, challenges still lie ahead. The historical evidence argues against ruling out recession, but any negative growth would be modest. After a dramatic 2022, bonds have remained volatile in 2023. Peak yields and slow growth would be positive for high-quality fixed income in 2024. As yields move lower, this would also support investor risk appetite and equity markets, but we expect material volatility in the first half of 2024.

Regardless of the jawboning by the Fed Chairman, interest rates should remain in place, at least through the first half of 2024. The ECB may be the first to lower rates mid-year, with the FOMC following in July 2024.

Equity Indexes in 2023 were strong but exceptionally narrow, as a few names accounted for almost all of the S&P 500 gains. Most diversified portfolios saw a massive difference in performance versus the index (unless investors owned an ETF that mirrored that index), leaving many investors needing clarification and support. This was mainly due to corporate earnings under pressure for most of 2023. There is room for recovery in the back half of 2024 as corporations have seen peak rates. Valuations are still above long-term averages due to the market expecting earnings expansion of around 12% and a 150 bps cut in rates. We see fewer rate cuts (75-100 bps) and lower earnings growth of about 6%. We should see improvement in profit margins (as companies tighten their belts over the last 18 months), and we have kept our forecast for next year’s valuations unchanged.

Monetary policy will remain the key driver in 2024. Still, we caution investors not to underestimate the risk from geopolitics, energy, the delicate relationship between the US and China, and the highly polarized US presidential election.

This would lead us to believe in high single-digit returns for equities in 2024, with higher volatility levels than we have seen in 2023.

Macro to Micro

Beyond our “macro view” – here is our “micro’ thinking as we move into the New Year.

We maintain a neutral overall risk stance in portfolios as we balance disinflation/recession and mixed economic data. If we moved into a mild recession, we don’t think it would cause additional volatility (we think the VIX will move higher regardless). We want to position for a range of economic and market scenarios and, by doing so, privilege portfolio diversification and quality of assets.

Peaking interest rates and a slowing economy should favor high-quality fixed income, offering diversification benefits to portfolios, particularly in volatile markets. We like intermediate-term government bonds, municipal bonds, and certificates of deposits (with less than two years of bank maturity).

The potential for a longer cycle of higher rates, limited corporate (re) issuance, and demand yields, we favor higher credit quality offered by investment grade bonds. Prudence is warranted for those who tinker in high-yield, as defaults should rise modestly.

As discussed earlier, we believe equities will end 2024 higher than they were when they began. However, we believe alpha will be delivered by those recognizing that volatility creates opportunity. Next year could see multiple corrections, and the rally/correction micro cycle(s) could frustrate investors without the cash to deploy. “Cash may not be king” next year, but it will be “a Bishop” to help when markets overreact (which they do in both directions).

Small-cap equities should be a part of investors' portfolios. We continue to hold a neutral stance but believe that many investors have left this asset class. That could be a mistake, as rate stability could help these companies' earnings in the new year.

A moderate recession or soft landing for the US economy amid sluggish growth elsewhere could see the US dollar (USD) maintain yield and growth advantages versus peers in 2024. However, a harder US landing would likely trigger safe-haven demand until the Fed responds with significant policy easing. The longer-term concern continues to be the private sector holding more treasury and dollars than central banks, which is a recent shift and something to watch.

With the recent rally in Gold (now above $2000 an ounce), we see short-term challenges to the commodity. We continue to like the asset longer term as Central Banks show no slowdown in buying bullion. Copper could see some medium-term support from tight supplies. OPEC+ will do everything it can to see Brent crude trade in a USD 80-90 range with continued cuts if necessary.

Hedge funds look positioned to benefit from return dispersion and volatility. For eligible investors, alternative investments can offer risk-controlled opportunities to participate in markets and/or hedged positions, taking advantage of market moves. Investors need to think of hedge funds differently than in years past; these investments are not to hit a 450-foot homerun (baseball analogy) but to hit singles and doubles in the gap (aka, fixed income plus like returns with less standard deviation).

Lastly, for qualified and institutional investors with an appropriate time horizon and risk tolerance, private assets can help diversify portfolios further and offer additional returns. We have seen private equity and venture capital find innovative companies in robotics, medical equipment, and the apparent advances in artificial intelligence. This is the space likely to find new disruptive and technologically innovative companies.

We wish you the Happiest Holiday this season and a very prosperous New Year.

Trade carefully. Thank you for listening.

Have a great week.

Stephen Colavito

Chief Investment Officer

San Blas Securities

stephen.colavito@sanblas-advisory.com

General Disclosures

This research is for San Blas Clients only. The opinions represented in this research are that of the CIO, not advisors or officers of San Blas Securities. This research is based on current public information that we consider reliable, but we need to represent it as accurate and complete, and it should not be relied on as such. The information, opinions, estimates, and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate. Some research can and will be published irregularly as appropriate in the analyst’s judgment.

This research is not an offer to sell or solicitation of an offer to buy a security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or consider our clients' particular investment objectives, financial situations, or needs (individual or corporate). Clients should consider whether any advice or guidance in this research suits their specific circumstances and, if appropriate, seek professional advice, including tax advice. Past performance is not a guide for future performance, future returns are not guaranteed, and a loss of original capital may occur. More information on San Blas Securities is available at www.sanblassecurities.com.