The Weekly Random Walk – August 28, 2023 From Stephen Colavito

An Aggregation of Various Economic, Market Research, and Data

53-Man Roster

This week, NFL teams must cut their 90-man rosters down to its regular season 53-man squad. The official deadline is Tuesday at 4 p.m. Although this represents the beginning of the regular season (football is back), it also presents a lot of players with the reality that their dreams of playing in the NFL come to an end.

Like the NFL, the regular season is about to begin. After Labor Day, Wall Street returns from summer vacation as kids return to school (yours truly became an empty nester last week), and we kick off the final leg of the 2023 trading year. We will continue to look at data to game plan how these markets may trade.

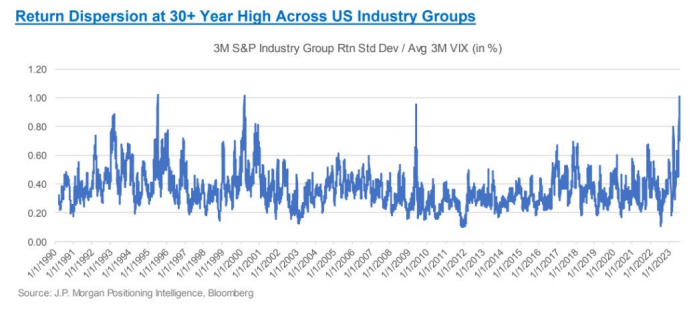

Spread Offense

While solid performance in the S&P 500 has dominated recent headlines, there is an even more substantial shift in performance taking place at the industry and sector level. Hot sectors include communication services, information technology, and consumer discretionary. Sectors that have lagged are interest rate sensitive, like real estate and utilities. These massive differences in performance YTD are like a spread office; this dispersion is near a 30-year high. We believe in mean reversion strategies and think utilities could outperform at the end of the Fed’s tightening cycle. Utilities in states that continue to see migration (Texas, Florida, Carolina, and Tennessee) benefit from more significant retail and commercial consumer bases.

Third and Long

This week, we had the chance to present to the Southeastern Accounting Conference, and we highlighted how the consumer is “behind the sticks” as savings are being depleted. Beyond our discussion, the Federal Reserve Bank of San Francisco issued a report last week estimating that if the current spending trend continues, the approximately 190 billion remaining in “aggregate excess savings would likely be depleted in the third quarter of 2023.” The US consumer has surprised the market with their spending resilience despite higher interest rates and economic slowdown. The chart below shows that excess savings generated from COVID-19 (which was extraordinary) are being depleted rapidly.

“Tampa Two” Defense

Housing has always been consumers' “zone defense,” as most of their net worth was in housing equity. As Fed Funds have climbed, so have the rate on a 30-year fixed mortgage as they have jumped to their highest level in 20 years. The Bankrate national average rose above 7.5% (30-year fixed mortgage), causing renewed worries about the impact on the housing market, which is already at the least affordable level in two decades. Higher rates may stall home sales, as existing homeowners are unwilling to give up their low-rate mortgages, and new buyers struggle to meet higher interest rate costs. This slowdown is already taking place. Mortgage applications have fallen significantly this year and are down 12% in the last seven weeks alone.

Since real estate prices (and equity) are supply and demand-driven, it’s a matter of time before home prices start to decline to get to an equilibrium for buyers based on location.

One more tidbit on housing. A systemic driver for higher housing prices has been a bidding war for properties with potential rental opportunities. This “AirBnB model” has created an artificial housing scarcity in popular tourist destinations. The tailwind behind the bidding war was 1) absurdly low mortgage rates and 2) post-pandemic price insensitive “revenge spending.” Both of those are over. This has made home prices for the bottom 90% almost impossible to afford—another reason why prices might decline in the future.

Second and One

Billionaires have no problem buying real estate. As reported in the New York Times this weekend, a group of Silicon Valley billionaires are behind the 800 million in land purchases outside of Travis Air Force Base in Solano County, California. So, if you have money burning a hole in your pocket, buying property around the AFB would seem like a layup when you have so much money buying around you.

Wide-Right

After the SVB collapse, many expected a wave of bank failures, much of which has been reverted. However, cracks have reemerged as Moody has downgraded ten small and mid-sized banks (note: always stay below the FDIC insurance limit).

Across a broader corporate landscape, we ran into this chart from Visual Capitalists showing that Chapter 11 and 13 filings are rising. Overstretched balance sheets and higher interest rates have added challenges for companies across sectors. So far, over 400 companies have missed their field goals wide right. Corporate bankruptcies are rising at the fastest pace since 2010, doubling the level seen last year.

Quick Hitters (Bullets)

Everyone expected NVDA to smoke their numbers, and they delivered. The expectation makes me think about what upside is left in the next few months. When I went to get a slice at my favorite pizza shop, and the guy behind the counter told me about buying NVDA because it’s “going to the moon,” we start to worry.

AI is real. After NVDA’s conference call, their demand for chips is evident. So, as long as NVDA can continue to increase its supply, there will be ample demand to gobble it up. So, in the long term, this theme is bullish for equities.

Chairman Jay Powell certainly gave the impression that the Fed will stay higher for longer. We don’t anticipate a rate hike in September, but if we continue to see unemployment remain in the mid-3s and inflation starts to increase (again), we expect another 25bps in November.

As we have argued previously, financial conditions are not restrictive, and it’s pretty clear in most of the data we have reviewed.

This leads us to believe that come September and October, equity markets might struggle. Valuations and the reality that rates are not coming down anytime soon would mean that markets have difficulty climbing higher. The S&P 500’s resistance point is 4600, so if we are lucky, the market bounces in the trading range of 4200-4600; if the data and earnings start to deteriorate in Q3, 4000 is not out of the question.

Next week, we hope to provide more details on the setup for the remainder of the year. But since we are tired from being in the 96F heat, we will call it a day.

Thank you for reading. We appreciate you. Trade and invest with caution.

Have a great week.

Stephen Colavito

Chief Investment Officer

San Blas Securities

stephen.colavito@sanblas-advisory.com

General Disclosures

This research is for San Blas Clients only. The opinions represented in this research are that of the CIO, not advisors or officers of San Blas Securities. This research is based on current public information that we consider reliable, but we need to represent it as accurate and complete, and it should not be relied on as such. The information, opinions, estimates, and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate. Some research can and will be published irregularly as appropriate in the analyst’s judgment.

This research is not an offer to sell or solicitation of an offer to buy a security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or consider our clients' particular investment objectives, financial situations, or needs (individual or corporate). Clients should consider whether any advice or guidance in this research suits their specific circumstances and, if appropriate, seek professional advice, including tax advice. Past performance is not a guide for future performance, future returns are not guaranteed, and a loss of original capital may occur. More information on San Blas Securities is available at www.sanblassecurities.com.